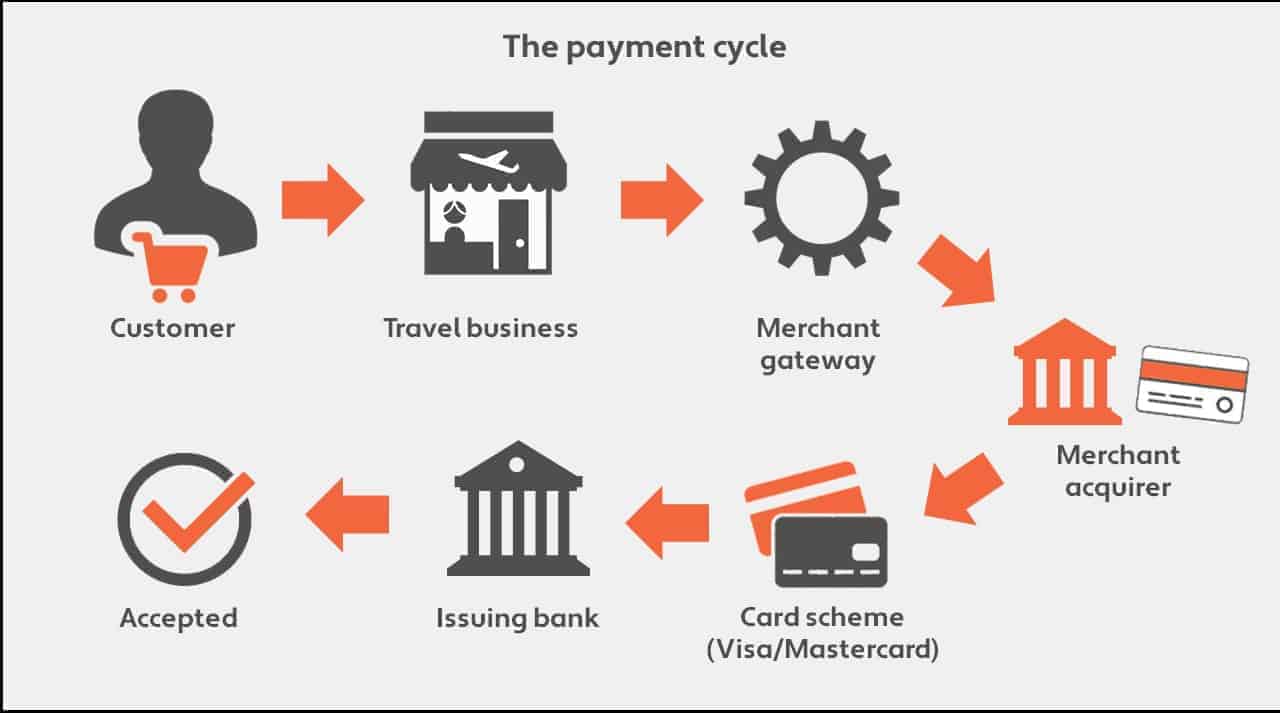

No business transactions are ever as simple as you think they should be. That’s certainly the case when it comes to accepting card payments. The process of charging a card is often over in a matter of seconds, but within that time it goes through several stages to reach completion. And one of them involves a merchant acquirer.

They are a vital link in processing debit or credit card payments, whether it’s online, through an in-store card machine or over the phone. Not only do they process the payment, but they also (most importantly) pass the funds to you within the terms you have agreed.

How do they make their money?

A merchant acquirer will charge you a fee, normally between 0.5% and 3%. The more transactions you carry out, the lower the charge. The fee often includes a variable interchange rate charged by the card issuer, someone like Visa or Mastercard.

There’s also another important element to your merchant acquirer’s fee structure. This takes into account their level of risk to chargebacks, which is regularly reviewed by risk committees who will require collateral from you as security.

The Chargeback scheme allows consumers to claim back money if a merchant hasn’t delivered on its contractual obligations to provide the goods or services purchased. If you go out of business, your merchant acquirer could be liable.

Why the travel industry is a special one

For merchant acquirers, the travel industry is a high-risk environment. There are several factors that contribute to this.

• The long timeframe between payment and delivery of the service increases exposure to chargebacks if anything goes wrong.

• Despite consumer protection through ATOL and other financial schemes in the event of a failure, credit card customers would be referred to the card provider by ATOL and ABTA to be repaid through the chargeback scheme.

• The current climate has increased the risk of travel businesses failing.

This hasn’t slipped the attention of the merchant acquirers who work with the travel industry. The biggest change you’ll notice is that they’re demanding a greater level of security. Some are even terminating their contracts with high-risk clients where additional collateral isn’t possible.

Some of our clients are being asked to provide collateral in one or more of the following ways:

• A deferred settlement, which might mean you have to wait longer to get paid. Instead of T+3 (3 days after the transaction), they might ask for T+7

• Rolling Reserves, where they hold back a percentage of the money, to limit their exposure (e.g. 10% for 3-6 months)

• Fixed Cash reserves in the form of an upfront cash bond (potentially substantial), which can be used for unexpected costs such as chargebacks

• A Trust Account, where the customer’s money is securely held until the holiday has taken place.

What this means for you

Finding this extra collateral can have significant cash flow implications for any travel business. It may also result in extra costs, such as those involved in setting up Trust Accounts. And all this at a time when every penny counts.

Travel Trade Consultancy supports businesses in their discussions with merchant acquirers to ensure the best possible outcome by:

• Introducing and assisting with negotiations

• Assessing the impact of the collateral and security demands from a cash flow perspective

• Providing support to your wider finance function

If you would like further information on any of the above, please get in touch.

If you enjoyed this post, why not sign-up to our newsletter? Get our latest blog posts, industry updates and exclusive content. Join our mailing list below.